You might think the ability to pay back debt would the most important criterion for borrowing money, but it’s not the only one, writes Campbell Korff.

A young couple came into the branch in Ballina the other day looking for a loan to finance their first home. After getting a little background on their income and savings, it was clear that their dream of buying a home was attainable financially.

However, ability to repay debt is not the only criteria used by most lenders. Lenders are also concerned to establish that a borrower has the willingness to repay as well. This sounds trite, but what they mean is that the borrower has demonstrated that they are sufficiently diligent and reliable to comply with credit terms over time. These days, this question is often answered by a statistical record known as a credit score.

Unfortunately for the couple in question, despite a clear record as far as defaults are concerned, they failed to reach the benchmark set by the many lenders who credit score. This is because their current bank had regularly offered them increased limits on their credit card as their financial situation improved. Ironically, this proved their undoing, because with each increase the bank lodged a “credit enquiry” on their credit record, negatively impacting their score.

While we were able to place them with a lender who doesn’t credit score, this narrowed significantly the number of lenders available to them and increased their borrowing costs.

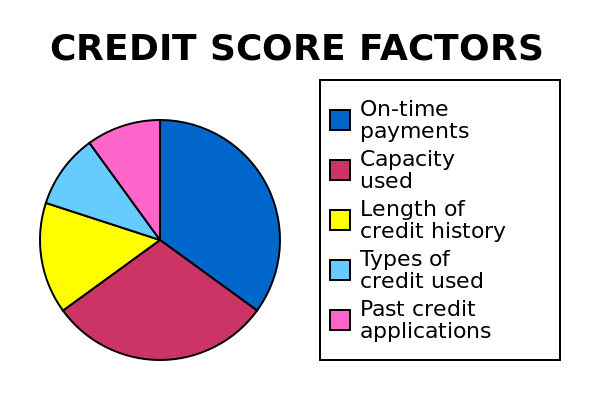

A credit score tracks your application for and repayment of debt. Obvious debt includes a mortgage, car finance and credit card, but phone companies and other utilities also run credit accounts.

“Their banks had offered them increased

limits which proved their undoing…”

A credit reporting agency receives information from finance companies, banks and utilities, and adds it to your credit file. Those things worth reporting include arrears on a bill (usually more than 60 days late), missed loan repayments, new applications for credit, guarantees, litigation, change of job and address and defaults. Most of this information remains on file for around five years.

While an agency collects your credit history and gives you a score, it’s the lender you are dealing with who makes the final decision as to what kind of risk you represent.

There are a few steps people can take:

- Clean up: start by getting your repayments organised for credit cards, bills and loans. You can’t change history but you can influence your financial future.

- Job and house: take the easy points on a credit score and don’t change address or job for a year before applying for a mortgage.

- Applications: try not to apply for unnecessary credit. Typically people that chase zero balance transfer rates and change their credit cards multiple times each year can get scored down, so be careful.

- Get a report: you can go to the web site of a reporting agency such as Veda to access your credit report. Once you know your score – and the reasons for it – you can start planning.

- Broker: some mortgage brokers provide a free credit report because it will help determine which lenders will consider your loan application. If you’re working with a mortgage broker, be sure to ask about this service.

- Build the positive: changes introduced this year mean you get to build a score on positive credit behaviour. This means that every on time repayment is a small positive mark on your credit file. It’s worth thinking about how to take advantage of this.

Credit reports are a fact of life if you want to borrow money – they can be really helpful, so learn how they work and start planning. Good luck.