The post Campbell Korff’s crusade against credit cards appeared first on .

]]>This Christmas I’m declaring a crusade against the credit card. I’ve had enough. Together with gambling, they’re a financial cancer eroding our national wealth. According to ASIC, we all owe the banks and other credit card issuers a total of around $31 billion. No, I’m not kidding.

Regular readers will recall my, now somewhat prescient, article in May 2015 on the Australian banks and the increasing pressures on their business model of borrowing short-term funds and lending (mostly home loans) for the long term. As I predicted, those pressures have negatively impacted their share price.

Well, no such pressures exist for credit cards. Despite record low interest rates, credit card rates have remained incredibly high. According to the RBA, the average cost of funds (interest rate at which they borrow) for the major banks is approximately 2.3%. While the average credit card rate is around 19%. That’s a profit margin of over 700%!

Yes, I know, there are 55 day interest free cards and others that give people the ability to better manage their cashflows, as long as they pay off the balance within 55days. Well, here’s the thing: the banks don’t issue these cards out of the kindness of their hearts. They issue them knowing that nearly all of us will regularly miss the interest free deadline and pay the ruinous interest and fees.

Canstar estimates that in the last four years we all paid a total of $35billion in credit card interest. That’s enough to pay off a quarter of the nation’s mortgages. What’s most frustrating about these statistics is that they are totally avoidable. Thanks to EFTPOS, debit cards and pre-paid travel cards, there is absolutely no need whatsoever to own a credit card. That’s right. No need whatsoever.

Many will argue that they need them to manage their cashflows each month. I can show you a far more effective tool that doesn’t cost you thousands of dollars each year: it’s called a budget and savings plan. All it takes is a little will power and patience and you will start growing your wealth, instead of destroying it.

If you don’t feel you can do this on your own, then drop me an email and I will show how to get off the credit card drug in months. No fee. No obligation. It will just make me feel good that my crusade has cancelled one credit card.

So go get the scissors out and start cutting up those cards before the financial cancer does any more damage to your wealth.

Contact Campbell Korff at Ballina Yellow Brick Road on: [email protected]

The post Campbell Korff’s crusade against credit cards appeared first on .

]]>The post Thinking outside the box – pricing for success appeared first on .

]]>Last week I was reviewing a client’s investment property portfolio and I was able to convince him that taking his negatively geared portfolio into retirement didn’t make a lot of sense and that it was time to shed one of them, so that the portfolio became positively geared.

I asked him what he would be willing to sell it for. Performing some mental arithmetic, starting with his purchase price and adding stamp duty, legal fees, rates and taxes and renovation expenses, he replied: “Well it owes me $750K, so around $900K seems right.”

While this seems compelling logic, it has nothing whatsoever to do with what his property is actually worth. His property is, of course, worth what the market is willing to pay him for it. His ‘sunk costs’ are irrelevant.

This cost-plus pricing fallacy is surprisingly common among both investors and businesses. A business owner making widgets might design Widget MkII, calculate its average cost of production, add his target margin and take it to market. Seems prudent, right? Wrong. The problem is that this ignores the impact of price on volume and volume on costs. A price increase to “cover” increased costs can start a death spiral in which higher prices reduce volumes and increase average unit costs even further, indicating (according to cost-plus logic) that prices should be raised again!

In simple terms, the cost to produce a widget is made up of fixed and variable costs. Instead of asking what price will cover total unit costs, the business owner should ask whether the change in price will result in an increase in revenue which is more than https://www.cialisgeneriquefr24.com/le-prix-de-cialis/ the variable costs of making the extra widgets (e.g labour, materials etc.). If the answer is yes, then the surplus is reducing fixed costs per widget and making the business more profitable.

Pricing is complex and dynamic and should be approached strategically and pro-actively as market circumstances change. Almost every modern household name you cialis tadalafil prix can think of (Apple, Netflix, Virgin, Aldi etc.) have been prepared to think outside the box on pricing and have profited by challenging the perceived wisdom. A good starting point, is to focus on what the customer is willing to pay (this can be improved with marketing, of course) and work backwards to production cost. When doing so, consider which fixed costs are sunk and, therefore, irrelevant to pricing. It’s pricing above the marginal cost of the next widget produced that counts.

Whether that’s a widget or an investment property, strategic pricing will result in higher profits. Email me at [email protected] if you would like more information.

The post Thinking outside the box – pricing for success appeared first on .

]]>The post Mark Bouris: Ten things young investors should know appeared first on .

]]>By the time you’re employed and receiving superannuation, you have an opportunity to invest for your future. It can be confusing and it shouldn’t be. So here’s 10 basics investment principles for those aged 30 and under.

Time: time is your second-greatest asset, after the ability to generate income. Time drives the compound effect, where returns on your assets are added-in to your lump sum. $1,000 that’s earning five per cent p.a. doubles in fourteen years thanks to compounding. If you’re a 25 year-old woman, you have another 70 years of living and letting compound interest work its magic.

Investment: don’t confuse investment with saving. Investment is developing an appreciating asset in the long term so it eventually generates income. Saving is accumulating cash for short-term goals such as house deposit, holiday, car and university fees.

Risk-Return: investing is a trade-off between risk and return, so to get high returns you take more risk (of the value going up and down) in assets such as shares. To ensure your returns, you have to stay invested for the long term.

Risk profile: the most important aspect of your profile is age. In your age group you have many decades to weather the ups and downs of share markets, so you enjoy the gains. Your greatest risk is probably inflation, which reduces the spending power of your cash by around 2.5 per cent each year.

Superannuation: super is not an asset class – it’s a tax-friendly investment vehicle that will deliver an income for you in your post-working years. Make sure you’re invested in super fund options that give you the best chance of building a large nest egg.

Property: if you can’t buy where you want to live, buy an affordable investment property and ensure it yields capital growth and income. There are tax-planning factors in property so model the investment with an accountant.

Goal: always create your own goals. It makes it easier to find the products, solutions and strategies relevant to you.

Advice: you don’t necessarily need full financial planning to gain expert insight. Some advisers will deal with you on an hourly basis and your super fund fees might include advice – use it!

Help: you don’t have to know everything. Try online apps such as Acorns and Self Wealth, which have smart options, at low cost without too much detail. To invest in shares without expertise, you can ‘buy’ the market: managers have funds that track stock exchange indices and you can buy exchange-traded funds (ETFs) that track indices of major stocks, such as the S&P ASX200.

Diversify: don’t place all your wealth in one asset, one asset class or one industry. Don’t overweigh yourself with for instance property, or mining shares – concentrated portfolios can fall faster and take longer to recover.

Finally, never take your eyes off inflation – the quiet destroyer. You can overcome the ‘risk’ of shares going up and down, by using time. But if you become too conservative and put all your money in cash, time allows inflation to win.

For more information on Yellow Brick Road, go to: https://www.youtube.com/watch?v=0K0C2F_DJLE

The post Mark Bouris: Ten things young investors should know appeared first on .

]]>The post Planners succeed, the rest hope they’ll get lucky appeared first on .

]]>I spent Friday afternoon with a good friend in Byron Bay. Over a long-ish lunch on a beautiful winter’s day, we sowed the seeds of what will become the succession plan for his business when he retires…20 years from now.

That seems ridiculously early to start planning your exit form a business, right? Wrong.

When you consider it has taken him 20 years to create and develop one of the nation’s leading data modelling businesses; which now employs 40 people and finely balances creative innovation with technical and analytical excellence (by no means natural bedfellows), I think his timing is impeccable.

From his point of view, at least, the business has reached its half-life and he wants to ensure that his legacy survives and is passed onto the next generation of stakeholders; whomever they might be.

The discussion began with him giving me a potted summary of the firm’s history, culture and people. As I gathered an insight into what makes his business tick so successfully, I began to wonder what common thread I could find in successful businesses generally which sets them apart from the crowd.

Yes, most tend to have passionate, hard-working principals at the helm. But, so do unsuccessful ones. Yes, they have a sound business model and high quality staff. But, I have also seen plenty of business fail with those attributes. Yes, they have a competitive advantage. But, we all know such an advantage can be fleeting. What I have found in common among the hundreds of businesses, large and small, which I have been involved with, is that the successful ones plan well, plan early and keep planning.

My friend’s business is at the cutting edge of ‘big data’. Just keeping up with the technological innovations in this space on a daily basis is breathtaking. Let alone trying to plan five, ten, twenty years ahead! So how does he do it?

Well, he doesn’t try to predict where technology will be in twenty years’ time. That is impossible and beyond his control. He assumes his business model and the products and services it produces will be in a constant state of evolution and plans around what he can control: people, culture, operations and capital structure. He figures if he has the best people working in a positive environment, where they have the resources they need and have a vested interest in the outcome, they will out-innovate and out-produce the competition.

This takes time and resources away from short-term revenue generation and may involve paying fees to expert consultants with no immediate dividend. Yet at the same time, it has created a business which is unusually resilient in a sector littered with the tombstones of great ideas that failed.

So, is 20 years too early to start planning his retirement? Not if he wants to maximise the value of his business for himself, his family and the stakeholders he leaves behind. Oh, and our next lunch is already planned.

Campbell Korff is a financial advisor. If you would like to contact him at Yellow Brick Road Ballina go to: www.ybr.com.au/Branches/Ballina

The post Planners succeed, the rest hope they’ll get lucky appeared first on .

]]>The post A fundamental financial fact – time is money appeared first on .

]]>If there is one concept of finance and investing which is at the same time the most important and the least understood, it would have to be the time value of money. It’s the fundamental building block that the entire field of finance is built upon. And yet, many people lack a solid understanding of how it works.

Time value of money is the economic principal that a dollar received today has greater value than a dollar received in the future. If you were given the choice between receiving $100 today or $100 in 10 years, which option would you take? Clearly the first option is more valuable because of:

Risk – There is no risk of getting money back that you have today.

Purchasing Power – Because of inflation, $100 can buy more Mars bars today than it will in 10 years; and

Opportunity Cost – a dollar received today can be invested now and earn interest. However, a dollar received in the future cannot begin earning interest until it is received. This lost opportunity to earn interest is the opportunity cost.

All time value of money problems are solved using two fundamental calculations: compounding and discounting.

Compounding is the process of determining the future value of an investment made today and/or a series of regular payments.

Most people understand the concept of compound growth. If you invest $100 today and earn 10% interest for two years, your initial investment will grow to $121 at the end of year 2. The initial $100 compounds because it earns interest on the principal invested, plus it also earns interest on the interest.

Discounting is the process of working out the value in today’s dollars of money to be received in the future, as a lump sum and/or as regular payments, by applying a discount rate. The discount rate is the required rate of return or opportunity cost of an alternative investment.

It is impossible to make a sound investment decision without using these calculations, yet few do so accurately.

To illustrate with a simplified example, if a property you want to buy is worth $500,000 today and you require a 10% return, assuming you hold it for 10 years and receive a yield of 2% after all expenses, you would need to sell it for around $1.1m in 2025. To help work out if that is realistic, you could discount back from today’s value to 2005 at the same rate of return and compare it to sales prices at that time.

There are obviously a lot of other variables to consider, so, as always, see a professional before you invest. It could save you thousands.

If you would like to learn more about prudent investing, please send me an email or drop in for a chat.

If you would like to contact Campbell Korff of Yellow Brick Road Ballina go to: www.ybr.com.au/Branches/Ballina

The post A fundamental financial fact – time is money appeared first on .

]]>The post Mark Bouris: Structuring your super for success appeared first on .

]]>

It’s a good time to remind ourselves that superannuation is not an investment – super is a tax and legal structure to create an income in your retirement.

Superannuation is a government regulated way to boost long term savings with generous tax concessions, as the mainstay of your retirement nest egg alongside your home. Your employer has to contribute 9.5 per cent of your wages into a complying super fund, and these contributions are taxed at 15 per cent, not the usually much higher marginal tax rate of your wages.

Once this money is in your account the earnings from the investment is taxed an average of 8 per cent. When you retire and draw down your lump sum, you pay zero tax on any earnings your investments then produce – another great benefit.

The price for all this is that once your money is in super, it is there until you retire.

The performance of your super really depends on the types of things (asset classes) you are invested in.

Growth assets like shares and property are more likely to produce shorter term fluctuations in their price. History has shown that shares have performed in this group over the past 100 years. But to get these returns you must invest for at least 10 years to weather the volatility they can create. This requires discipline, calmness and the ability to stay focused on the long term result above the noise of today.

At the other end of the spectrum, putting your money in cash is a more stable. But when interest rates are low – as they are now – you risk losing your earnings to inflation. Generally you need to aim to produce an overall return from your super after tax and fees that is two per cent to four per cent a year better than inflation to enjoy a decent retirement. Adding in more than the regulated 9.5 per cent of wages is also required.

In between cash and equities, there are fixed interest investments such as government, corporate debt and property. They are more volatile than cash but don’t have the same returns as shares.

Where should your super be invested? Match your planned retirement length to the asset classes that will produce enough income for that time. For a 65 year old today this is at least 20 years. In the past, people would switch to cash or fixed interest from any growth investments they held which is seemingly prudent but it is very dangerous as it maximises the impact of your number one risk. That risk is that you run out of money too early or have to live on much less than you would like.

A better way is to simply place one to two years of income into cash and bonds in a separate account. This means you have immediate living expenses covered for a few years, while your nest egg is growing and the price moves around in the short term.

The main point to remember as the super statements arrive: Super is not the investment, but you can actively manage your investment options within super to ensure you gain the best returns commensurate with your timelines.

If you would like to contact Campbell Korff of Yellow Brick Road Ballina go to: www.ybr.com.au/Branches/Ballina

The post Mark Bouris: Structuring your super for success appeared first on .

]]>The post Campbell Korff on why it pays to have your glass half full.. appeared first on .

]]>It’s a well known face that we fear loss two to three times more than we enjoy gains. This psychology explains a lot of our behaviour in everyday life. Indeed, it has been critical to our survival for thousands of years.

Risk aversion can be very important when hunting for food in foreign environments, constructing a dwelling and caring for our young. However, when it comes to investing in the modern world it can lead to chronic underperformance. Here are a few reasons why:

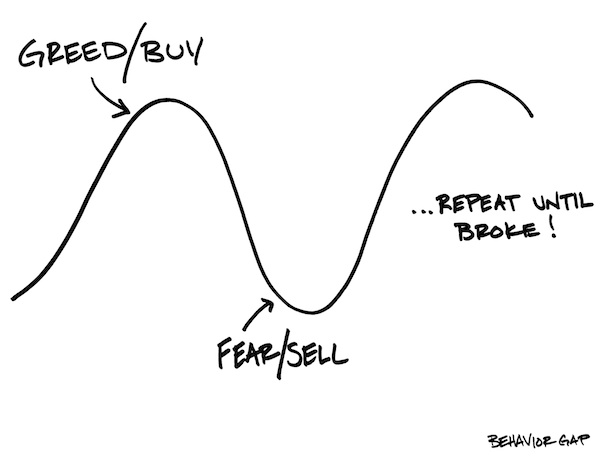

Procrastination – fear of loss causes us to put off financial decisions in the hope tomorrow will be a better day. The problem for pessimists is that day may never come or be so delayed that more damage is done by leaving their capital on the sidelines.

Financial media – if we all felt great about the economy and our financial security we would never pick up a financial newspaper or watch the finance news each night. Our inherent financial insecurity has created a multi-billion dollar industry expert at exaggerating the most obscure financial data so long as it feeds our inherent belief that the financial world might just end tomorrow and send us all bankrupt.

Ignoring the facts – it is a fact that the Australian stock market has delivered average returns in the high single digits for over a century. It is also a fact that over this period only around 1 in 5 years produced negative returns. If you invested $10,000 in the Australian Stock Market in 1980 and re-invested the dividends, these facts would deliver you an investment worth around $850,000 today. You don’t believe me, do you? Our fear of loss causes us to discount positive data even when we know it’s true.

Short term thinking – we invest our savings across our entire adult lives. For most of us, this is a 60 to 70 year timeframe. Yet how often do we make decisions based on short term data? The Australian stock market is down around 15% since April, which is not good news if you need to sell your entire share portfolio tomorrow. If you don’t, history indicates it is more probably a time to think about investing more.

Compounding losses – there’s only one thing worse than losing money; that’s throwing good money after bad! Even when we know we have made a bad financial decision, we often stick our head in the sand in the hope the losses will miraculously disappear, rather than exit and stop the bleeding. Everyone makes mistakes. Face them, learn from them and move on.

Our fear of loss is instinctive, which makes it very hard to displace. However, to be successful investors we must be aware of how it can cloud our judgment and filter out information which is designed to accentuate this fear, rather than help us make good investment decisions.

If you would like to contact Campbell Korff of Yellow Brick Road Ballina go to: www.ybr.com.au/Branches/Ballina

The post Campbell Korff on why it pays to have your glass half full.. appeared first on .

]]>The post The silver lining in the major bank rate rise appeared first on .

]]>The ‘Big Four’ banks all took the unusual step a couple of weeks ago of raising their mortgage rates by between 0.15 and 0.20% independently of the central bank. While by no means welcome news for homeowners, already nervous about a fragile economy, the rise will have a modest impact given the low base they rose from.

What the rise is really about, is the banks’ need to raise capital to sure up their balance sheets following APRA’s change to its capital adequacy requirements for banks in July this year. Obviously, if you are in the business of selling new shares, it is best to do it at a time when the prospects for future growth in earnings are good. If this is not the case, all you are doing is diluting existing earnings (from which dividends are paid) among more shareholders. The result: a lower share price.

For many reasons the opposite is currently true for the Big Four banks. So demonstrating to the market that they retain pricing power and are able to maintain their earnings, even in an unfavourable environment, will help the sales pitch for their new shares. For the time being at least.

The real winner out of this move is the RBA and, ultimately, the broader economy. Hitherto, the RBA was between a rock and a hard place: it needed to maintain low, possibly lower, interest rates to support a rebalancing of the economy but at the same time take the steam out of an over-heated metropolitan property market. Ongoing constraints in the supply of new homes and limited influence on lending policies, made this task almost impossible.

Fortunately, in an unintended act of altruism, the Big Four have raised rates and signalled that they might do so again. They have also had to, belatedly, tighten their lending to property investors. This has sent buyers in Sydney and Melbourne back to their spreadsheets.

Thus, the way is now clear for the RBA to maintain, if not further reduce, the cash rate to support the services sector and exporters (who will benefit from a resultant lower dollar). All good news for the Northern Rivers economy.

If you want to contact Campbell Korff of Yellow Brick Road Ballina go to: www.ybr.com.au/Branches/Ballina

The post The silver lining in the major bank rate rise appeared first on .

]]>The post Campbell Korff on planning your exit strategy to maximise value appeared first on .

]]>

Small business underpins our economy and provides a source of income and store of wealth for millions of Australians, writes Campbell Korff. This means that those same Australians also rely on the value realised from the sale of their business to support them in retirement – and that can be a problem.

I have discussed previously how not enough small business owners are making use of the huge tax advantages of superannuation during their working lives. All is not lost, however, if you are in this category. The government anticipated this and has provided small business owners with special tax concessions when they sell their business assets at retirement, provided they then make use of superannuation.

What this all means is that it is critical that business owners maximise the value of their businesses when they sell out or retire.

For most, however, this means seeking offers a few months before they need to sell from their own network or possibly getting a local real estate agent to do some advertising. Having negotiated a quick deal with a competitor or staff member, a short meeting with their accountant and solicitor follows to work out the tax bill and contract.

Where was the planning? Looking before your leap is probably a good idea…

Given most small business owners put their heart and soul into their businesses for most of their lives, this process hardly seems to be doing justice to a life’s work.

Where was the planning? What was the valuation method? What steps did the owner take in the years leading up to exit to maximise that value? Was a sale the best exit or would more value be captured by structuring a succession plan for a promising junior? Were other structures available to entice the buyer to pay more? Was a tax and retirement plan developed beforehand?

Exiting a business successfully is a complex process during which hundreds of thousands of dollars of your wealth can be destroyed if care and, importantly, expert advice is not taken well ahead of time. Indeed, to a certain extent, you should always be buyer ready because you never know when that ‘too good to refuse’ offer might land on your desk.

If you want to contact Campbell Korff of Yellow Brick Road Ballina go to: www.ybr.com.au/Branches/Ballina

The post Campbell Korff on planning your exit strategy to maximise value appeared first on .

]]>The post Win $5000 and a mentoring session with Mark Bouris appeared first on .

]]>

Verandah Promotion

Do you want to meet renowned Australian businessman, media personality, chairman of Yellow Brick Road, and this seasons host of Celebrity Apprentice, Mark Bouris?

Yellow Brick Road Ballina are offering you the chance to meet with Mark Bouris for a one hour mentoring session where you can get Mark’s personal insights into being successful. They are also throwing in a hefty $5,000*

For your chance to win, register with Mark’s trusted advisers at Yellow Brick Road Ballina for an obligation-free 15 minute financial health check.

In your financial health check, your advisor will look at what your financial goals are, where you are now and help to start you on your journey to a secure financial future.

Contact our Ballina branch on 02 6686 6678 for your obligation-free health check and we can get you started on your path to financial freedom.

* Competition Terms and Conditions apply. Credit services provided by Yellow Brick Road Finance Pty Limited ACN 128 708 109, Australian Credit Licence 393195. Financial Planning services provided by Yellow Brick Road Wealth Management Pty Limited ACN 128 650 037, AFSL 323825.

The post Win $5000 and a mentoring session with Mark Bouris appeared first on .

]]>